-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

李文君女士 (Judy Li)

分析師

畢業於香港科技大學並取得工商管理碩士學位。曾在相關產業和家族辦公室等公司任職。具有股票分析和投資經驗。現為輝立証券持牌分析師,主要負責化學、醫美和消費等板塊的研究工作。

分析師

畢業於香港科技大學並取得工商管理碩士學位。曾在相關產業和家族辦公室等公司任職。具有股票分析和投資經驗。現為輝立証券持牌分析師,主要負責化學、醫美和消費等板塊的研究工作。

| Phone: | 22776515 | Email: | judyli@phillip.com.hk | |

Satellite Chemical Co., Ltd. (002648.SZ) - An integrated production enterprise in the light hydrocarbon industry chain, performance continues to improve

Tuesday, December 12, 2023  749

749

Satellite Chemical Co., Ltd.

| Recommendation | Buy |

| Price on Recommendation Date | $15.410 |

| Target Price | $19.320 |

Weekly Special - 3306 JNBY Design Limited

Overview

The company stands as a leading integrated manufacturer in China's light hydrocarbon industry chain, primarily focusing on three core fields: functional chemicals, new polymer materials, and new energy materials. It boasts ownership of the first imported ethane comprehensive utilization unit, the pioneering propane dehydrogenation unit, and China's largest acrylic production facility. Its extensive product range includes HDPE (high-density polyethylene), EO (ethylene oxide), EG (electro-galvanizing), SAP (super absorbent resin), polyether macromonomer, hydrogen peroxide, and other products. These products hold a prominent position in various sectors such as aerospace, new energy vehicles, electronic chips, agriculture, forestry maintenance, healthcare, and more.

Company performance review

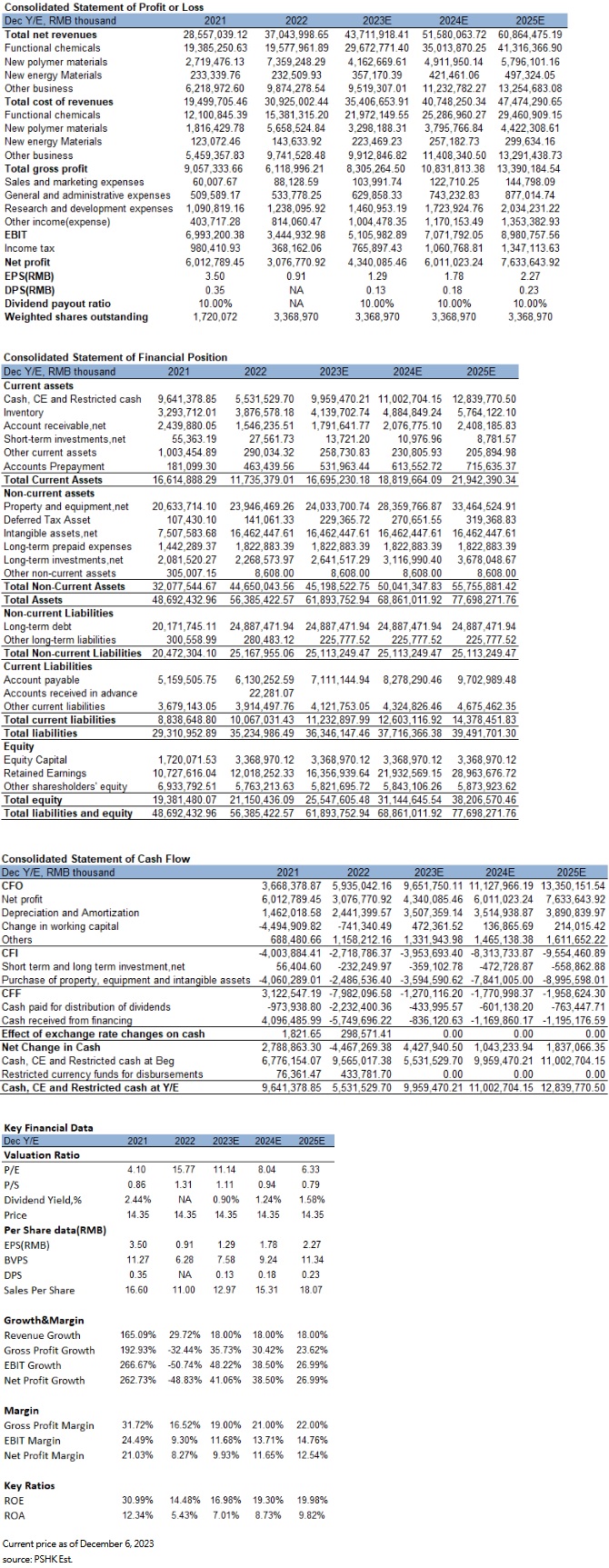

In 2022, the company experienced notable dynamics in its financial metrics. Sales revenue surged to 37.044 billion yuan, marking an impressive year-on-year increase of 29.72%. However, despite this revenue uptick, the net profit attributable to shareholders of listed companies witnessed a significant decline, plummeting to 3.062 billion yuan, a staggering 49.02% decrease compared to the previous year. Similarly, the net profit attributable to shareholders, excluding non-recurring gains and losses, fell to 3.044 billion yuan, reflecting a substantial year-on-year decrease of 47.98%. These declines in profitability metrics were accompanied by contrasting trends in margins. The gross profit margin experienced a noticeable drop, decreasing by 15.20 percentage points to 16.52%. Simultaneously, the net profit margin saw a decline of 12.77 percentage points, settling at 8.27%. Despite these challenges, the company's total assets by the end of 2022 rose to 56.385 billion yuan, showcasing a commendable year-on-year increase of 15.80%. The earnings per share amounted to 0.91 yuan, with the company's decision not to distribute cash dividends. The primary factor contributing to the revenue surge but profit decline can be attributed to the substantial increase in raw material prices, particularly ethane, throughout 2022. This surge in costs, combined with pressure on selling prices due to insufficient demand for major products, led to a situation where the rise in product costs outpaced the revenue increase, resulting in a decline in the gross profit margin year-on-year.

Main business analysis

The company's core operations center around two pivotal industrial chains: C3 and C2. The C3 industrial chain is dedicated to propylene and downstream products such as acrylic acid and acrylates. Propylene is produced via the PDH (propane dehydrogenation) catalytic reaction within this chain. The PDH method, leveraging clean raw materials and straightforward processes, offers notable advantages—low investment threshold, high product yield, superior quality, and clear cost efficiencies. The accessibility of propane compared to ethane has attracted a surge of domestic PDH players, rapidly expanding production capacity. However, this amplified supply has led to an overall decline in profits within the propane-propylene linkage. Consequently, the focus on profit within the PDH project has shifted towards downstream deep-processing products. Currently, propylene's downstream applications encompass various fields including polypropylene, propylene oxide, acrylonitrile, butyl octanol, and acrylic acid. Distinct profitability trends have emerged among different PDH projects since 2021. Projects supporting acrylic and those utilizing propylene oxide have showcased stronger profitability, while those supporting polypropylene have displayed relatively weaker performance. Notably, the company's provision of acrylic acid and its million-ton acrylic acid industry chain positions it uniquely, establishing a competitive edge in the PDH industry. The C2 industrial chain involves ethane cracking to produce ethylene, polyethylene, among other products. The company's C2 business utilizes imported ethane as its primary raw material and incorporates an ethane cracking device. This method overcomes the limitations of traditional ethylene production methods characterized by high energy and material consumption and low ethylene yield. In contrast to naphtha cracking and coal-to-ethylene processes, this approach offers advantages like a streamlined process flow, reduced device investment, and higher ethylene yield.

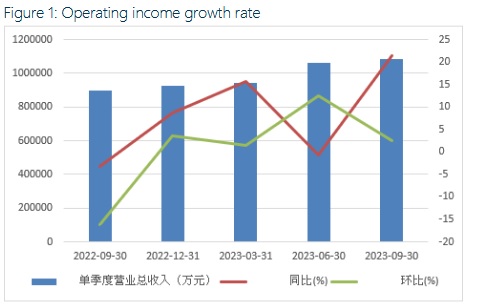

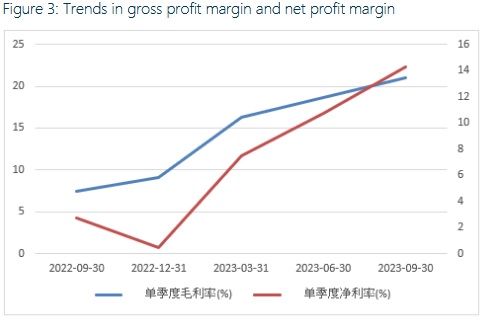

During the first half of 2023, the company recorded promising financial figures. The operating income reached 20.014 billion yuan, marking a 6.38% year-on-year increase. However, the net profit attributable to the parent company declined to RMB 1.843 billion, down by 34.13% year-on-year. Non-net profit also experienced a decrease, settling at RMB 1.952 billion, reflecting a 28% year-on-year decline. The gross profit margin, at 17.51%, saw a year-on-year decrease of 6.97 percentage points, while the net interest rate stood at 9.20%, down by 5.64 percentage points compared to the previous year. Breaking down the performance in the second quarter, the company observed mixed results. Revenue was 10.599 billion yuan, exhibiting a marginal year-on-year decrease of 0.72%, yet indicating a substantial month-on-month increase of 12.57%. The net profit attributable to the parent company in this quarter was 1.136 billion yuan, showcasing a 9.87% year-on-year decline but a noteworthy month-on-month surge of 60.59%. Achieved non-net profit stood at RMB 1.17 billion, marking a 1% year-on-year increase and an impressive 51% month-on-month increase. Additionally, the gross profit margin in the second quarter was 18.62%, down by 2.37 percentage points from the previous year but exhibiting a substantial month-on-month increase of 2.35 percentage points. The net profit margin settled at 10.71%, experiencing a year-on-year decrease of 1.1 percentage points but showing a robust month-on-month increase of 3.22 percentage points.

In the initial half of 2023, revenue from functional chemicals totaled 10.247 billion yuan, marking a 7.46% decrease year-on-year but a notable 20.49% increase month-on-month. The gross profit margin stood at 15.04%, reflecting a substantial 15.9 percentage point decrease from the previous year but a positive 5.91 percentage point increase compared to the prior month. On the other hand, revenue generated from polymer materials amounted to 5.606 billion yuan, exhibiting a remarkable 97% year-on-year surge and a concurrent 24.22% increase from the previous month. The gross profit margin in this segment was 27.74%, declining by 7.2 percentage points year-on-year yet experiencing a robust 12.09 percentage point increase month-on-month. Furthermore, new energy materials revenue reached 139 million yuan, showcasing a 27% year-on-year rise and a 12.42% increase compared to the previous month. The gross profit margin for this sector was 31.70%, indicating a year-on-year decrease of 6.3 percentage points and a month-on-month decrease of 6.71 percentage points.

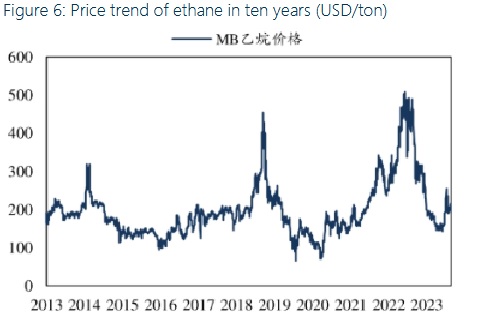

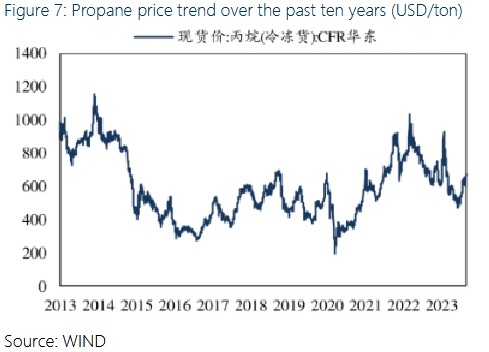

The company has seen an improvement in performance for two consecutive quarters, attributed mainly to the gradual decrease in prices of primary raw materials. Baichuan Infu reported that the average propane price in the first half of 2023 hit US$617/ton, marking a substantial 25.89% year-on-year decrease and a 9.08% decrease from the previous month. In the same period, the average ethane price reached US$167/ton, signifying an immense 53.08% year-on-year drop and a staggering 50.91% decrease month-on-month. During the second quarter of 2023, various price differences surged: the polypropylene-propane difference by 2,354 yuan/ton (a 50.57% month-on-month increase), the polyethylene-ethane difference by 6,677 yuan/ton (a 1.29% month-on-month increase), and the ethylene oxide-ethane difference by 4,598 yuan/ton (a 3.12% month-on-month increase). This rise in profit is primarily attributed to declining prices of the company's raw materials, propane and ethane, and the balancing of product price differences.

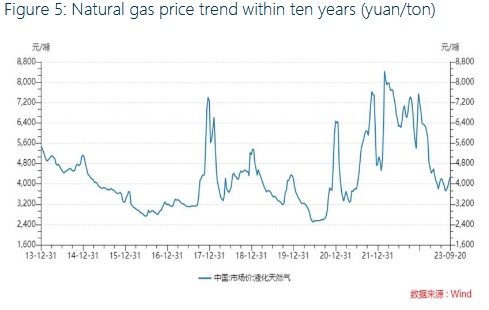

Following September 2023, both ethane and propane prices have surged. The ethane/Brent crude oil price ratio reached the 33rd percentile within the past decade, while the propane/Brent crude oil price ratio stood at the 26th percentile over the same period. Ethane, as a component of natural gas, can serve as a direct energy source. Its price typically correlates positively with natural gas prices. Recent trends in natural gas prices have been notable. In Asia, indicative prices for natural gas hit a five-month high in August, while Europe experienced a two-month peak. This surge in prices has been primarily driven by extended periods of hot weather, especially in the United States, along with supply constraints caused by labor disputes in Australia, a key producer. These factors have tightened the supply-demand dynamics, exerting upward pressure on natural gas prices. Currently, the price of natural gas stands at 3835 yuan/ton after a recent rise from a lower level. The "China Natural Gas Development Report (2023)" by the National Energy Administration forecasts a steady rise in demand. Influenced by economic conditions and both domestic and international natural gas price trends, it's estimated that national natural gas consumption in 2023 will reach 385 billion to 390 billion cubic meters, reflecting a year-on-year increase of 5.5% to 7%. This growth is primarily attributed to increased usage in urban gas and power generation. In the short term, with the escalation in prices of ethane and propane, it's anticipated that profits from ethane cracking and PDH units will experience a slight contraction.

The U.S. Energy Information Administration (EIA) forecasts a gradual rise in natural gas prices over the next few years. Predictions indicate a decrease to $2.58 per thousand cubic feet by 2023 (previously estimated at $2.62) and a subsequent increase to $3.22 by 2024 (down from $3.29). Despite this upward trajectory, the pace of increase is expected to be slower. Industrial demand growth is anticipated to boost natural gas production, reaching 102.98 billion cubic feet per day in 2023 and further increasing to 104.13 billion cubic feet per day in 2024. This production growth in the United States will fuel an ongoing supply of ethane to meet market needs. Contrarily, in Europe, decreased consumer spending has led to accumulating finished product inventories, curbing demand for industrial gas and thereby pushing natural gas prices down. This scenario is expected to maintain lower prices for both natural gas and ethane. Analyzing price differences in the C2 and C3 industry chains, ethane cracking to ethylene price differences narrowed in September. Currently, apart from HDPE/DMC (polyethylene/molding plastic), which returned to mid-to-high levels, most downstream products in the C2 industry chain remain historically low. Meanwhile, in the C3 sector, prices for propylene, polypropylene, acrylic acid, and butyl acrylate increased while PDH spread narrowed. However, overall downstream product price differences in the C2/C3 industry chain are still historically low. As the overall price difference between the C2/C3 industry chain gradually recovers in the future, the company's profitability is expected to improve.

Valuation and recommendation

The company anticipates the operational launch of its Pinghu base new materials and new energy integration project by the end of 2023. This strategic initiative aims to enhance efficiency in utilizing PDH's propylene resources, producing multi-carbon alcohols through projects like 360,000 tons of acrylic acid, 720,000 tons of ester technological transformation, 300,000 tons of polypropylene, and 250,000 tons of hydrogen peroxide. This endeavor forms a closed industrial chain focusing on propylene-acrylic acid-acrylate.

Market data from Baichuan Yingfu reveals China's actual acrylic acid consumption, which surged to 2.415 million tons in 2022, marking a significant 23.4% year-on-year increase, with a five-year CAGR of 10.3%. The industry's concentration, notably with a CR5 proportion of 60.9%, underlines its high consolidation. Satellite chemistry, commanding an 18.9% market share, stands as the industry leader.

In terms of research and development (R&D), the company's commitment is evident. In 2022, R&D investment surged by 15.14%, amounting to 1.238 billion yuan. The company's innovation drive resulted in 107 patent applications, a 50.70% year-on-year increase, with 93 patents authorized. Moreover, in the first half of 2023, R&D expenditure escalated by 9.74%, totaling 708 million yuan. During this period, the company applied for 50 patents and secured 51 authorized patents. Notably, successful developments in α-olefin industrial test devices and POE devices have positioned the company at the forefront of the domestic α-olefin field.

The company has ambitious plans, intending to invest 25.7 billion yuan to establish a high-end new materials industrial park, focusing on comprehensive α-olefin utilization in Xuwei New District, Lianyungang. Negotiations are underway for a ship leasing agreement with SINOGAS or related parties to support the project's raw material supply. This strategic expansion aims to fortify the company's industrial chain advantages, envisioning it as a premier domestic supplier of high-end polyolefin products by establishing an α-olefin integrated base.

Based on the company's substantial reserves in ongoing projects, gradual future growth is anticipated. Projected revenues of 43.712 billion yuan, 51.580 billion yuan, and 60.864 billion yuan from 2023 to 2025, with a compound annual growth rate of 18.00%, are forecasted. Anticipated earnings per share (EPS) are 1.29/1.78/2.27 yuan, with corresponding price-to-earnings ratios (P/E) of 11.14/8.04/6.33x. The company's average P/E over the past three years stands at about 17.64. With a forecasted 15 times P/E in 2023 and a valuation of RMB 19.32, we recommend a "buy" rating. (Current price as of December 6)

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()