-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Jinko Solar (688223.SH) - A leader in TOPCon solar cell, benefiting from the rapid growth of overseas PV module demand

Monday, September 19, 2022  1097

1097

Jinko Solar(688223)

| Recommendation | Buy |

| Price on Recommendation Date | $17.360 |

| Target Price | $21.230 |

Weekly Special - 3306 JNBY Design Limited

A Brief introduction to the company

Jinko Solar(688223.CN) is a worlding-leading and vertically-integrated photovoltaic module company. Founded in 2006, the company has formed an integrated business of silicon ingots, silicon wafers, PV cells, and solar modules. The company's revenue mainly comes from the sales of modules. In the first half of 2022, the company achieved module shipments of 18.92GW, ranking first in the world.

A review of 2022 H1 Results

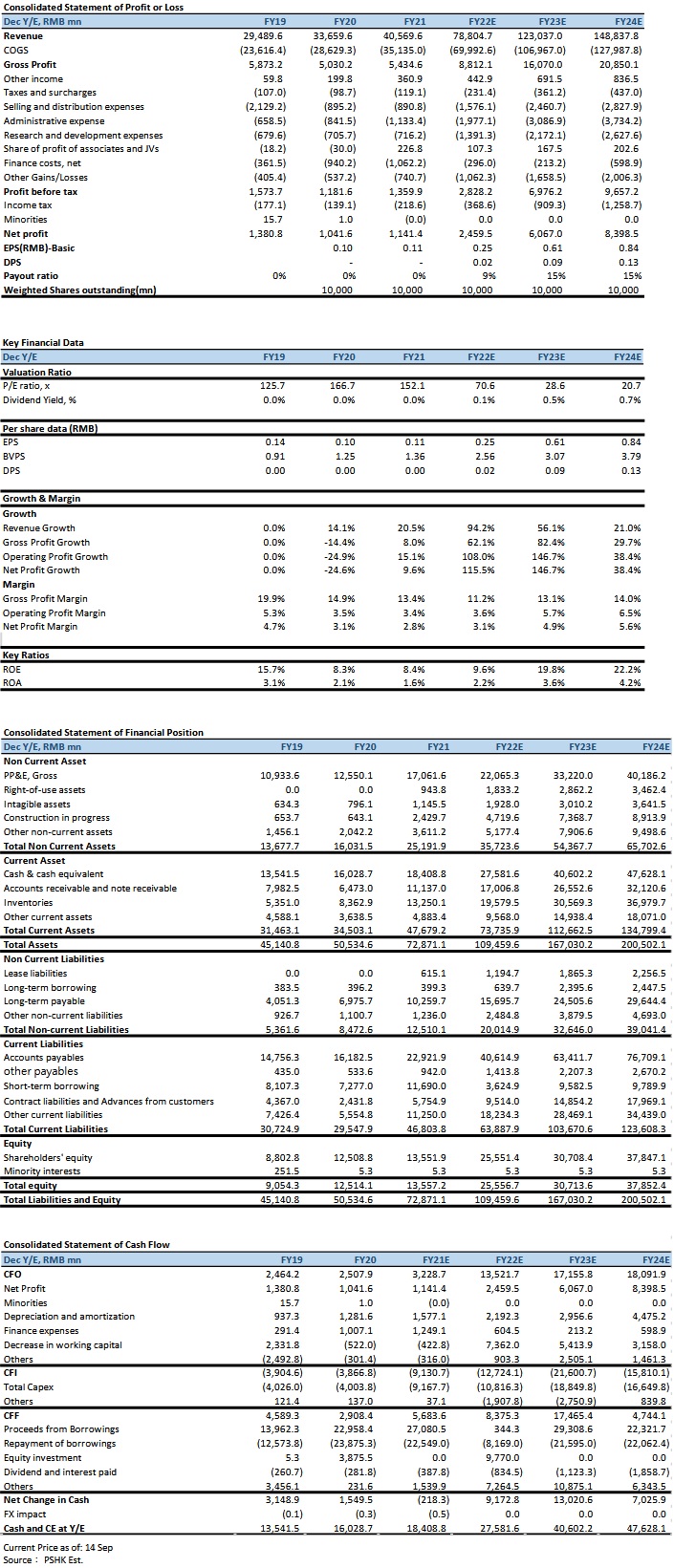

The company has announced its 2022 semi-annual report. The company achieved an operating income of 33.41 billion yuan (RMB, the same below), up 112.4% YoY, with revenue in Q2 being 18.73 billion yuan, up 138.8% YoY, and up 27.5% QoQ. The net profit attributable to shareholders was 910 million yuan, up 60.1% YoY, with net profit attributable to shareholders in Q2 being 500 million yuan, up 55.5% YoY, up 25.6% QoQ. Net profit attributable to shareholders after deducting non-recurring gains and losses was 800 million yuan, up 299.2% YoY, with the number in Q2 being 503 million yuan, up 55.5% YoY, and up 67.3% QoQ. The GP margin was 10.25%, down 4.09% YoY, with the margin in Q2 being 11.20%, down 4.29% YoY, and up 2.16% QoQ. The substantial increase in the company's revenue and profit was mainly due to the significant increase in the company's PV product shipments to 18.92GW, a YoY increase of 79%, of which PV module shipments reached 18.21GW, ranking first in the world. In addition, the proportion of the company's sales revenue in the European market increased significantly from 19% to 27%, mainly due to the substantial increase in demand in the European photovoltaic market this year. The company expects Q3 module shipments to be 9-10GW, and 35-40GW for the full year.

Due to the strong PV module demand, PV manufacturers have significantly raised their PV module shipment expectations for 2022-2023

As the Russian-Ukrainian war is reaching a stalemate, European natural gas imports have been slashed, and European electricity prices have risen sharply. In addition, the European Commission launched the RepowerEU plan and the EU Solar Strategy, and plans to install more rooftop PV modules, resulting in a substantial increase in the installed PV capacity in Europe. Mr. Li Zhenguo, the general manager of LONGi Green Energy, pointed out that the demand for photovoltaics has exceeded expectations. The market originally believed that the installed PV capacity in 22/23 was 250/350GW, but now it is likely to be close to 300/400GW. In addition, Trina Solar expects to add about 280-300GW of installed capacity in 22 years and 380-400GW in 23 years, far exceeding the market's original expectations. Therefore, we believe the company continues to benefit from the substantial growth in demand from the photovoltaic industry.

Jinko focuses on developing ultra-efficient N-type TOPCon technologies, ahead of its peers

With the PV industry experiencing a transition from P-type PV technology to a more photoelectrically efficient N-type PV technology, the market is now paying attention to the most economical N-type TOPCon PV cell technology (at least in short term). Compared with the N-type HJT battery, the N-type TOPCon cell technology can utilize the existing PERC production line, so the production cost per watt of the cell is lower than that of the HJT battery. The company insists on focusing on developing highly-efficiency TOPCon PV cells, as a result, its TOPCon production capacity has been greatly increased. As early as 2019, the company built a TOPCon battery production line and its mass production efficiency in 2020 reached 24.2%, creating a first-mover advantage. Subsequently, the company built 8GW Hefei and 8GW Haining production lines, with a mass production conversion efficiency of 24.8%. By the end of 2022, its planned production capacity of TOPCON cells will reach 35GW, ranking first in the industry. From a technical point of view, the company's TOPCon technology ranks first in the world. The company's self-developed 182 N-type TOPCon cell has a conversion efficiency of 25.7%, having been certified by the Chinese Academy of Metrology, setting a world record for the highest TOPCon cell conversion efficiency. The company expects that the second phase of the TOPCon production line will produce TOPCon cells with a mass production conversion efficiency of 25% in 2022, continuing to lead the industry in the coming years. Therefore, we expect the company continues to deliver PV modules with the lowest levelized cost of electricity(LCOE, a measure of photovoltaic cost per kilowatt-hour) in the industry, and the market share of the company's PV modules will increase from about 13% in 2021 to 18% in 2024, approaching to a market share of 20-25% rate target.

Jinko is now increasing the production capacity of silicon wafers and cells, reducing the cost of PV modules

PV Module manufacturers` profits have been decreasing due to upstream wafer and cell price increases, so module manufacturers are now deploying a vertical integration strategy, penetrating the silicon wafer and PV cell industries, to ensure stable profits. The company understood that its silicon wafer and battery production capacity is insufficient and is now deploying the integration strategy. As of the end of 2021, the company's wafer/cell/module production capacity is 32.5/24/45GW, revealing that the production capacity of wafers and cells is in shortage and the degree of vertical integration is insufficient. To solve the shortcomings of silicon wafers and cells, the company plans to have a production capacity of 60/55/65GW of silicon wafers/cells/modules by the end of this year. As the company becomes more vertically integrated, we expect the company's gross margin volatility to decrease.

The company has a high proportion of overseas business, and it is expected to benefit from the explosive growth in Europe

The company is committed to expanding its global production, logistics, sales, and service network to meet the needs of customers around the world. As of the second quarter of 2022, the company's products and services cover more than 160 countries. From the perspective of the regional structure of revenue, the company's overseas revenue accounted for 74% in the first half of 2022, of which 27% came from Europe. We expect that overseas markets (especially the European market) will continue to benefit from the rising energy prices and policy support, and the company is expected to benefit greatly from the explosive growth of the foreign PV market due to the high proportion of business in overseas markets.

Company valuation

We believe that the company has the advantages of TOPCon PV cell technology and vertical integration, and the company has greatly benefited from the explosive growth in Europe due to the high proportion of overseas business. We expect that the company's module business will usher in explosive growth and its market share will increase substantially and the company will continue to rank first in PV module shipment. In addition, the degree of integration of the company continues to rise, and we expect the company's earnings stability to increase, which is beneficial to the company's long-term development. We predict that the company's EPS in 22/23 will be ¥0.25/0.61 respectively, up 115%/147% YoY, corresponding to 70.6/28.6x price-earnings ratio (P/E) in 22/23. Since the company's EPS growth rate is much higher than that of peers, we believe that the company's valuation should be much higher than its peers` stock value, giving the company 35 times PE in 2023 and a target price of ¥21.23, with a "buy" rating. (Current price as of September 14)

Risk factors

1) PV demand falls short of expectations; 2) Technology substitution risks, such as HJT, and perovskite cell development exceed expectations; 3) Raw material cost declines less than expected; 4) Market competition intensifies; 5) Production capacity falls short of expectations; 6) Trade barriers.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()